Shenzhen on Both Sides of the Front

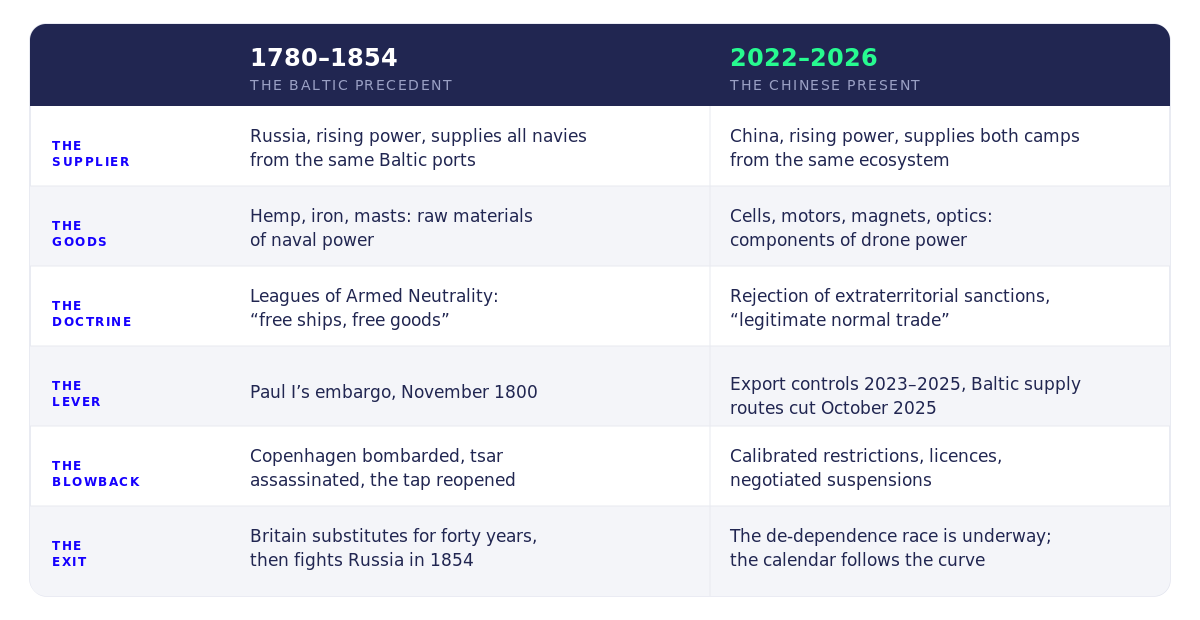

Both camps of the drone war run on the same Chinese supply chain. The Royal Navy spent fifty years rigged in Russian hemp: history says the winners are those who build the substitution layer before the tap closes.

Both camps of the drone war buy from the same supplier. The Royal Navy knew the feeling.

This is the third post of our defense series. The first mapped the European defense-tech landscape and its capital structure. The second described the productive-forces shock: the drone has displaced the shell, and the material base of war has moved to consumer electronics. This one traces that supply chain to its owner, and asks what history says about wars fought on an industrial base controlled by a rising power. The answer points to where European founders should build.

A first-rate ship of the line carried 50 to 100 tons of hemp in its rigging, cables and sails, to be replaced every one to two years. In 1801, 86% of the hemp Britain imported came from Russia, and by one historian’s estimate the Royal Navy would have ceased to function within eighteen months had the supply stopped. The fleet that policed the world’s oceans, the instrument of British hegemony, floated on the commercial goodwill of a rising rival power. Britain knew it, Saint Petersburg knew it, and for half a century both sides priced that knowledge into every diplomatic crisis in the Baltic.

The reader of our previous post will recognize the situation. The FPV drone that now inflicts the majority of casualties on the Ukrainian front is assembled, on both sides, from the same Chinese consumer-electronics ecosystem: roughly 80% of the electronics in Russian drones is Chinese according to a senior NATO official speaking in October 2025, and nearly 89% of Ukraine’s drone-related imports by value came from China in the first half of 2024, per the Snake Island Institute. One supplier, two clients, one war. The eighteenth century ran the same experiment, at length, and documented the results.

The riser’s arsenal

Russia in the eighteenth century occupied the position China occupies today: a continental power recently arrived in the concert of nations, converting scale into leverage over established powers. By the 1770s it had overtaken Sweden as the world’s largest iron exporter, peaking at some 62,000 tons exported in 1782, roughly a third of world pig iron at century’s end. It held a near-monopoly on the hemp, flax and mast timber without which no fleet could sail. And it supplied every navy at once. While the Royal Navy rigged itself at Riga and Saint Petersburg, French agents bought the same naval stores in the same ports, shipped home under neutral flags. The two fleets that fought each other from Ushant to the Chesapeake were, upstream, customers of the same warehouses.

Russia also supplied the doctrine. The Leagues of Armed Neutrality that Catherine II assembled in 1780 and Paul I revived in 1800 asserted the right of neutrals to trade with all belligerents: free ships make free goods, contraband confined to actual weapons, blockades valid only if physically enforced. London, which ran the eighteenth-century equivalent of secondary sanctions through its prize courts, treated the doctrine as a mortal threat. Beijing’s position on extraterritorial sanctions since 2022 is the same text with new nouns.

The tap, turned

The one full-scale test of the lever came in 1800. On 18 November, Paul I embargoed British trade, seized around 200 British ships in Russian ports and interned four to five thousand sailors. The effect registered within weeks: a documented hemp crisis, panic at the Admiralty, some £19 million spent on emergency grain imports in a country already stressed by bad harvests. The Cabinet’s response was to order the Baltic fleets of the League destroyed piecemeal, and Nelson bombarded Copenhagen on 2 April 1801. By then the crisis had already resolved itself by other means: Paul had been assassinated in his bedroom ten days earlier, on the night of 23 March, and the news had simply not yet reached the fleet. His son Alexander lifted the embargo in May and the League dissolved.

The episode established two facts that every subsequent supplier of both camps has had to weigh. The lever was real: a paper decree in Saint Petersburg degraded the world’s dominant navy faster than any French squadron ever had. And pulling it fully proved fatal to the man who pulled it, because a hegemon confronted with an existential input cutoff escalates rather than folds. China has read the file. Its restrictions since 2023 are calibrated, reversible and priced: export licences rather than embargoes, suspensions negotiated at summits, and an 87% price increase on export-controlled dual-use goods sold to Russia between 2021 and 2024, against 9% for other customers. The modern supplier monetizes the chokepoint rather than closing it.

Shenzhen on both sides of the front

The current numbers deserve to be laid out layer by layer, because the dependence is not one number but a stack of them.

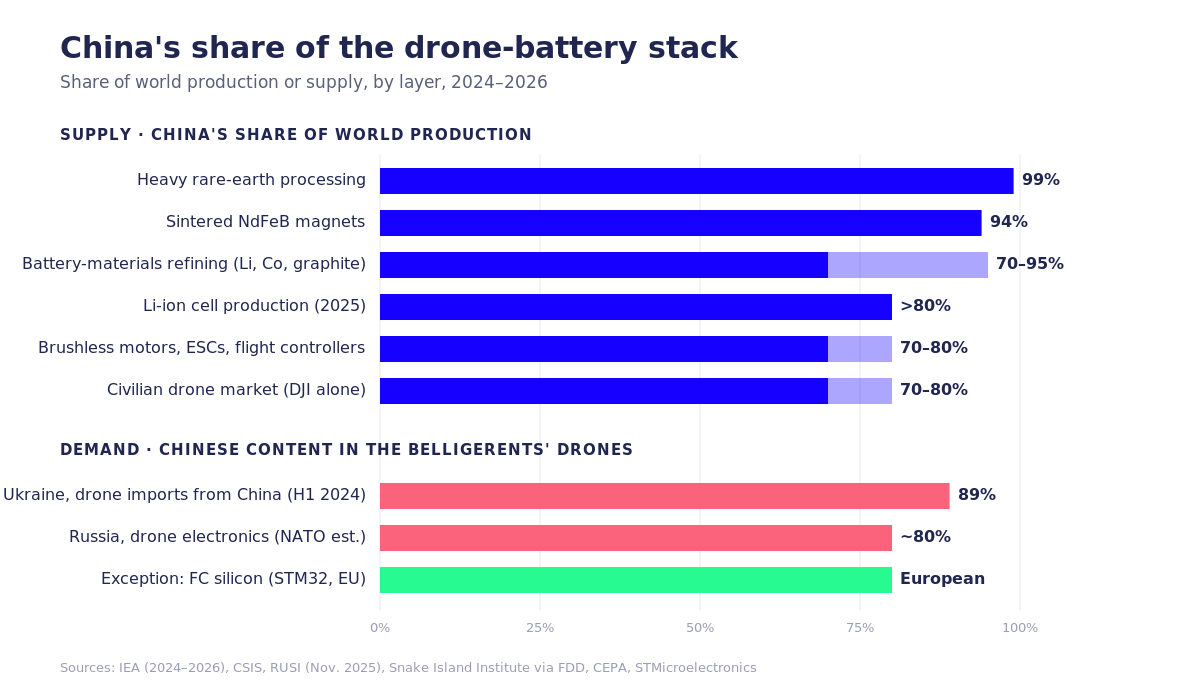

DJI alone holds roughly 70 to 80% of the global civilian drone market. In October 2023, Ukraine’s then prime minister Denys Shmyhal claimed his country was buying 60% of DJI’s global Mavic output; DJI disputed the figure, noting that Shmyhal had no insight into its production numbers, and nobody disputed the underlying point, which is that Ukraine’s eyes on the battlefield were at that time and are still for a very large part made in Shenzhen. Chinese manufacturers account for 70 to 80% of world sales of brushless motors, speed controllers and flight controllers. China produced over 80% of the world’s lithium-ion cells in 2025, refines 70 to 95% of the lithium, cobalt and graphite behind them, and makes about 94% of the world’s sintered rare-earth magnets, with a 99% grip on heavy rare-earth processing. There is no layer of the FPV bill of materials, apart from the silicon itself (the flight controllers mostly run on European STM32 chips), where China is not the reference supplier for both belligerents.

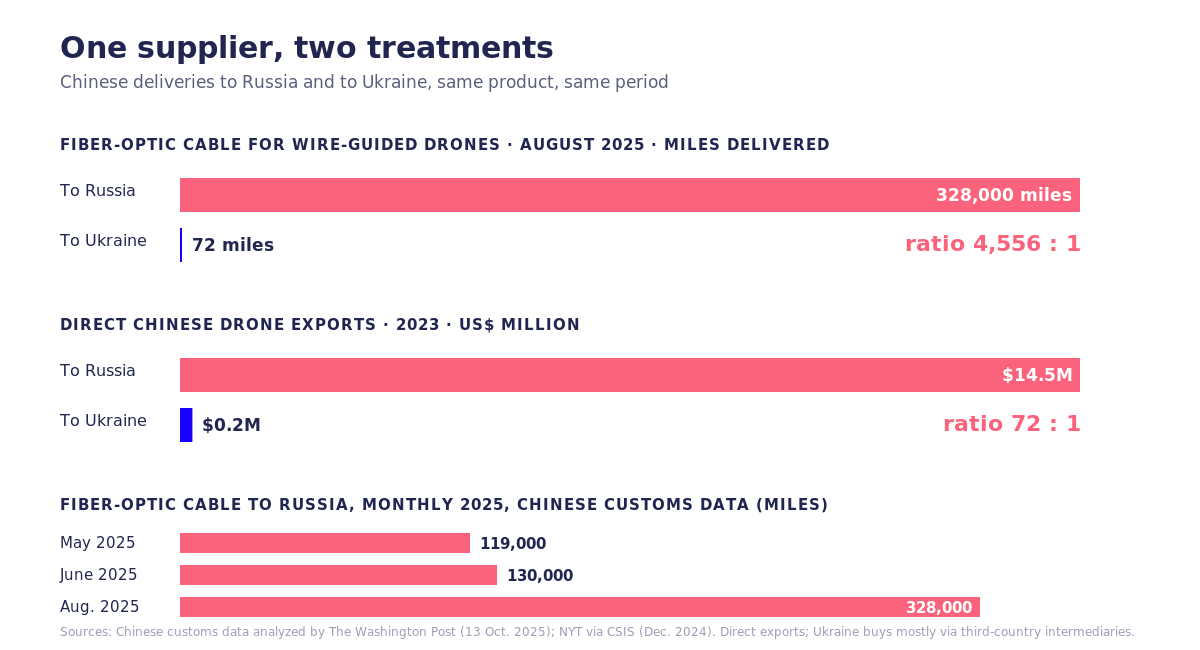

What distinguishes 2026 from 1800 is the asymmetry of the flows. Russia is served; Ukraine is squeezed. In 2023, direct Chinese drone exports were $14.5 million to Russia against $0.2 million to Ukraine (source CSIS). In August 2025 alone, Russia imported 328,000 miles of Chinese fiber-optic cable for its wire-guided drones, according to Chinese customs data analyzed by The Washington Post; direct shipments to Ukraine that month came to 72 miles. Ukraine buys most of its Chinese fiber through third-country intermediaries, which is precisely the point: the 4,500-to-1 gap measures Beijing’s trade policy, not Ukraine’s consumption. The same customs data put Chinese lithium-battery shipments to Russia at a record $54 million in June 2025, and Reuters documented Chinese engines reaching Russia’s Garpiya attack-drone line in crates labelled “industrial cooling units” after sanctions hit the first supplier, with more than 6,000 aircraft contracted for 2025 against 2,000 the year before. President Zelensky put it plainly in May 2025: the Chinese Mavic is open to the Russians and closed to the Ukrainians. In October 2025, Beijing went further and cut component sales to the Baltic states and Poland, the identified transshipment routes to Ukraine, a move Catherine II would have recognized as blockade enforcement by the supplier itself.

The West is itself a target of this leverage. When Beijing sanctioned Skydio, the largest American drone manufacturer, in October 2024, it cut off the company’s single Chinese battery supplier and forced it to ration customers to one battery per drone for six months. When the April 2025 rare-earth controls landed, Chinese magnet shipments to the euro area were down roughly 75% year-on-year by May, according to the European Central Bank, and production lines stopped at Ford in Chicago and at suppliers in Germany and Austria. A single licence regime in Beijing now reaches into the assembly halls of the American and European defense industrial base, which is precisely the position London woke up to in December 1800.

How Britain actually escaped

Britain escaped by making hemp matter less, never by out-producing Russia, and the timeline deserves attention because every step happened under duress, none by foresight. Iron chain cables were trialled on a merchant ship in 1808, tested by the Admiralty in 1810 and adopted from 1812, removing the single largest consumer of Russian cordage. Mast imports from the Baltic collapsed from 17,000 to 4,600 in 1808 under Napoleon’s blockade, and Canadian supply rose from 4,422 sticks before the war to 23,053 by 1811, with the Navy Board paying a substantial premium over the Baltic price to build the alternative. Manila abaca displaced Russian hemp as the world’s premier cordage fiber only when the Crimean War cut the Russian supply outright. And when Britain finally did fight its supplier in 1854, the fleet it sent into the Baltic was the first major British force to sail entirely under steam.

The substitution took forty years, and it was still incomplete: in 1854 Britain absorbed 60% of Russia’s hemp exports and two thirds of its flax, and the allied blockade of Russia was deliberately designed to let through the raw materials London still needed, rerouted overland through Prussia. Two lessons for the present. Substitution is the work of decades even for a motivated hegemon, and it begins in earnest only when the crisis makes it unavoidable. And the strategic calendar follows the dependence curve: Britain permitted itself a direct war against Russia only once the chokepoint on its fleet had been engineered away.

The substitution layer

For a European founder looking at this structure, there are three possible postures, and they are not equal. Replicating the Chinese component base head-on is a capex trap: a brushless motor is a scale business, and the scale is in Guangdong. Stockpiling and rerouting is a trading business with trading margins, not a venture case. The venture case is the third posture, the one Britain eventually found: building what makes the Chinese input substitutable or non-critical. We call it the substitution layer, and Ukraine has spent three years demonstrating, under fire, what it looks like layer by layer.

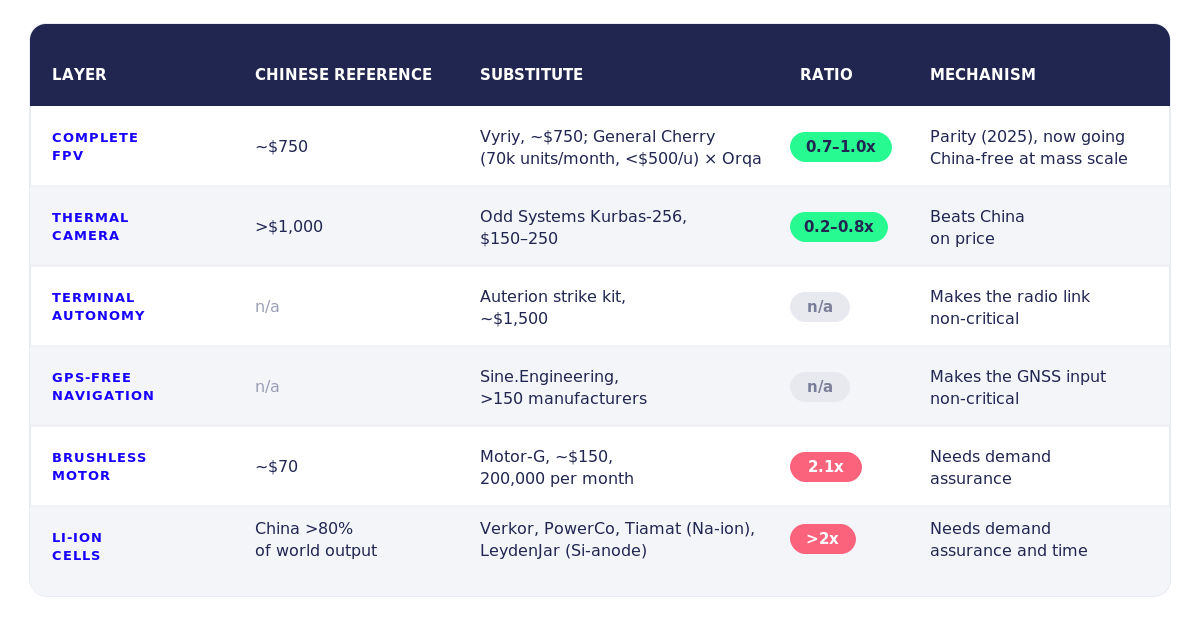

Ukraine crossed a milestone in March 2026: it can now produce drones containing no Chinese components at all, printed circuit boards included. Kyiv’s stated goal is telling: the guaranteed capacity to keep producing if Beijing cuts everything, rather than full localization, which remains years away at mass-production scale. That capacity is the exact definition of the layer. Within that effort, the economics differ sharply by component, and the differences are the investment map.

The pattern in the table is the thesis. Where the value sits in engineering rather than in manufacturing scale, parity with China is already achieved, and sometimes exceeded: Vyriy sells its China-free FPV at the Chinese price, Odd Systems sells its thermal camera below it, Sine.Engineering built its GPS-free navigation business without raising outside capital. General Cherry, one of Ukraine’s largest drone manufacturers, already produces more than 70,000 FPV drones per month, with systems priced below $500 and credited with over $1B of Russian equipment destroyed. It is now pursuing the same objective of eliminating Chinese components through a strategic partnership with Croatia’s Orqa, whose drone stack is already entirely China-free, to build a concealed manufacturing facility in Ukraine (press release). The cheapest substitution of all moves the criticality to a layer where the monopoly does not exist, instead of remaking the component. An autonomy kit at roughly $1,500 (Auterion’s Pentagon contract prices 33,000 strike kits at $50 million) raises FPV hit rates from the 10 to 20% range to 70 to 80% and makes the drone indifferent to the radio link that Chinese jammer-resistant hardware would otherwise dominate. Software-defined anti-jamming does the same for the radio link itself, at a fraction of the cost of hardened military radios; it is one of the layers where we are spending our diligence time. Fiber-optic guidance removes the RF layer entirely, and Ukrainian firms now wind their own spools even while the raw fiber still comes from China.

The business-model question

The honest objection to all of this is price: how does a European component maker live against a supplier whose reference price is 30 to 50% lower? Part of the answer is above: pick the layers where engineering beats scale, or move the criticality. But two further arguments change the comparison itself.

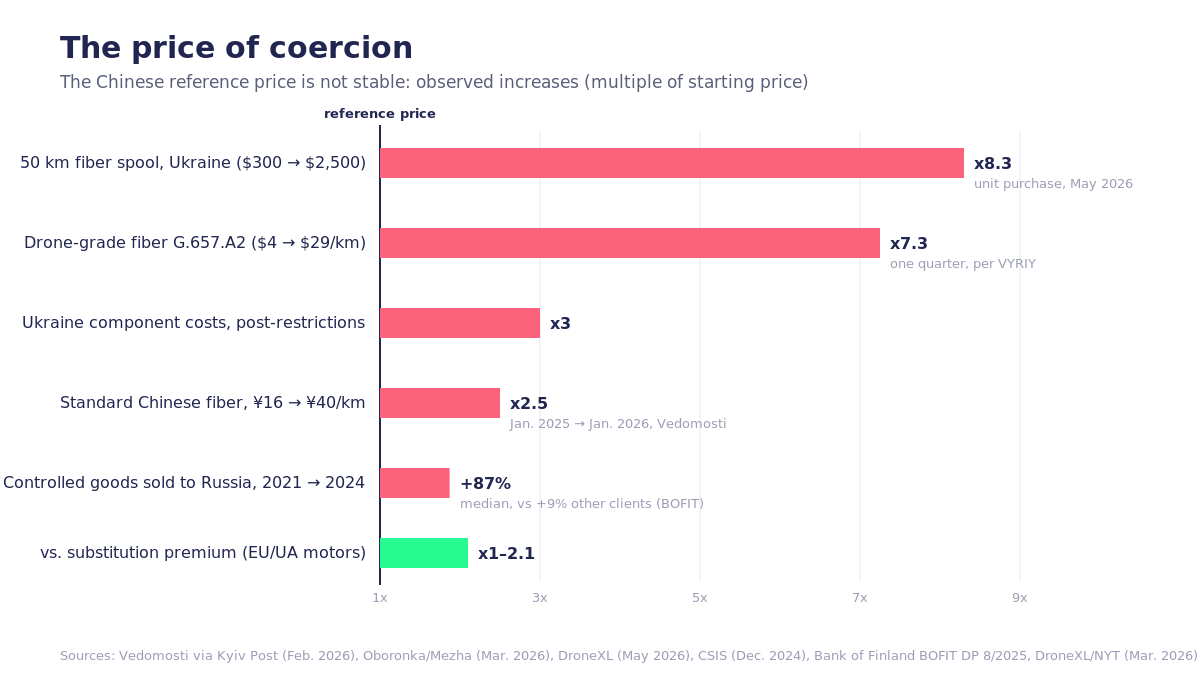

The first is that the Chinese reference price is a spot price that now embeds a coercion premium, and the premium is rising. According to the Russian business daily Vedomosti, relayed by the Kyiv Post, the average price of a kilometer of standard Chinese fiber-optic cable went from 16 yuan ($2.33) in January 2025 to 40 yuan ($5.83) in January 2026. That is the generic benchmark; the bend-insensitive G.657. A2 fiber that combat drones actually fly on went from roughly $4 to $29 per kilometer within a single quarter, according to the Ukrainian manufacturer VYRIY, and one Ukrainian drone unit reported paying $2,500 for a 50 km spool that cost $300 a year earlier (more information). Ukrainian component costs tripled after the 2023–24 restrictions. Russia itself, the favored customer, has paid a median 87% markup on export-controlled goods since 2021, against 9% for China’s other clients, per a Bank of Finland (BOFIT) study. The correct comparable for an investor is the risk-adjusted price of the Chinese input over the life of a defense program, and on that basis the substitution premium of 1x to 2x is cheap insurance. The 1801 precedent prices the alternative: adjusting after the tap closes cost Britain a subsistence crisis, a bombarded neutral capital and a murdered tsar, followed by forty years of the same substitution work it could have started earlier.

The second argument concerns the state, because the question “can founders do this without the EU?” has an empirical answer from Kyiv. Where parity is reachable, private capital suffices: Vyriy and Odd Systems needed customers, not subsidies. Where a structural cost gap persists, as in motors and cells, the effective public instrument is demand assurance rather than production subsidy. Ukraine’s rule since March 2025 is simple: any manufacturer exceeding 50% localization by component value becomes eligible for guaranteed state contracts of three, five or ten years. The buyer pre-pays resilience, exactly as the Navy Board paid the Canadian premium on masts after 1808. Europe has the budgets, and it even has localization rules: EDIP’s €1.5 billion programme for 2025–27 puts more than €230 million into calls targeting unmanned systems and drone-electronics supply chains, and both EDIP grants and SAFE’s €150 billion in procurement loans carry a 65% European-content requirement. What is still missing is the demand-side conversion. EDIP’s threshold conditions subsidies; SAFE’s conditions individual contracts; the new European Military Sales Mechanism aggregates demand without guaranteeing any. No EU rule yet converts a localization threshold into contracted revenue over time. Europe pays for localization; Ukraine contracts for it. For founders, this defines the play: reach parity where engineering allows it, and position on the layers where the guarantee mechanism, when it arrives, will find you as the qualified European source. It arrived in Ukraine within three years of the first Chinese restriction. Crisis-driven, as procurement reform always is.

The window, again

We closed our last post on the observation that every doctrinal reform of the twentieth century was crisis-driven, and that investors who underwrite structural exposure early arrive ahead of institutional resolution. The supply-chain version of that argument now has a date attached. Britain fought its supplier only in 1854, once the substitution was done; the strategic calendar of the West’s confrontation with China can likewise be read in the de-dependence curve, and both Washington and Beijing know that the supplier’s leverage peaks now, while the curve is still flat. For the European founder, the same clock runs the other way. The years in which the Chinese input is still cheap, the coercion premium still rising, and the European demand-assurance mechanism still unbuilt are the years in which the substitution layer can be claimed at seed prices. Nelson’s fleet was rigged in the rival’s hemp for fifty years. Nobody who owned the substitutes regretted it.

Previous posts: Who owns Europe’s next arsenal? · After the shell

This article was written with the help of Claude (Anthropic).

To continue the discussion, share your feedback at francois@newfundcap.com.