What happens to the secondary market when the top 5 names IPO?

The secondary market that has been building over the past few years is about to reset. It is time to assess what worked, what didn't, and what strategy best captures the durable value of the market.

The venture secondary market just crossed an annualized $112 billion in the first quarter of 2026, the first time it has outrun the public listing market, according to Pitchbook. Every headline treats this as a new asset class coming of age. Look closer at the composition and a different picture appears. Five companies drive nearly half of it.

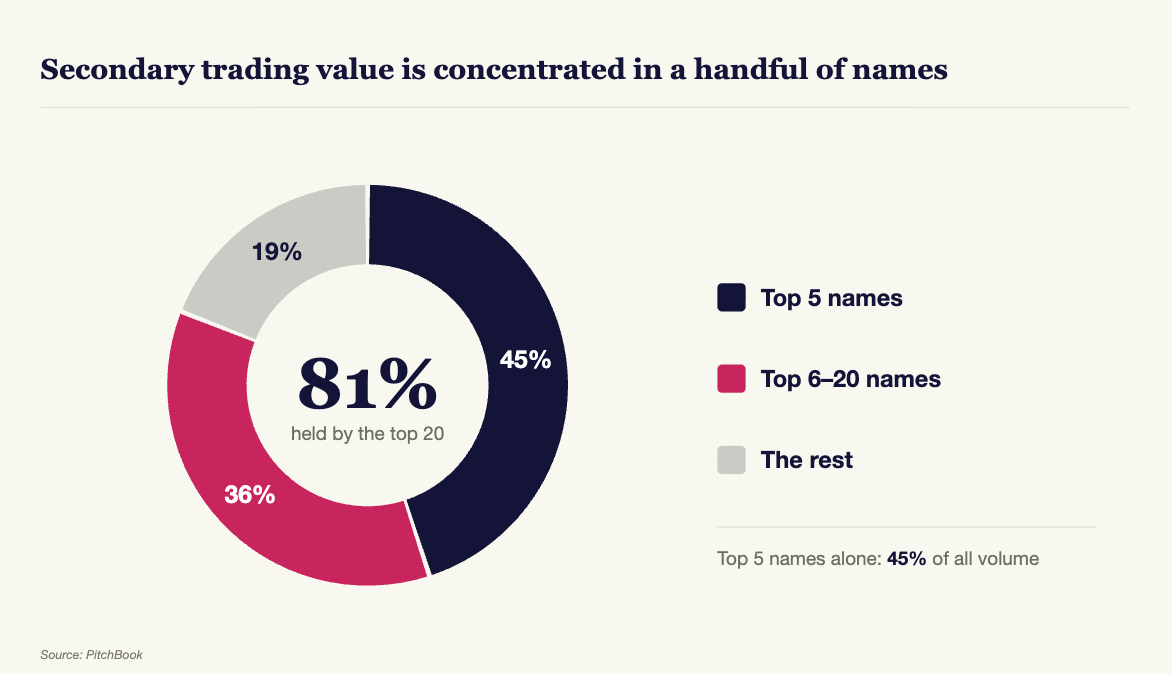

The current secondary market concentration

Twenty names account for 81% of all secondary trading value. The top five alone, SpaceX, OpenAI, Anthropic, xAI, Anduril, account for 45%. Three quarters of SPVs with carry point at that same short list.

A market where five names move half the volume is a market that grows when those names are in fashion and it contracts when they leave. It is the exact definition of a wave, and this wave is breaking.

The break on the horizon

SpaceX listed last month and then acquired xAI. OpenAI and Anthropic have both filed confidentially. The secondary demand that piled up around these names are about to disperse and reset the secondaries market.

What remains after these IPOs is a shallower pool of companies with shorter track records, fewer bidders competing for them, and prices that are far harder to set. Capital that was parked in pre-IPO secondaries will look for its next home after lockups period end, and the churn starts again around whichever names are fashionable in the next six months.

The appetite for private-market exposure will stay stable. The object of the appetite will keep moving.

This concentration breeds problems

To buy the fashionable names, most investors go through special-purpose vehicles, and the structures have grown baroque. SpaceX demand produced SPVs stacked four and five layers deep. Each layer charges and half the gain evaporates into the stack before it reaches the investor.

Ownership is another problem in the SPV fiasco. Companies such as OpenAI, Anthropic, and Anduril restrict share transfers. So, many buyers through these vehicles never even hold the underlying stock and cannot confirm what they actually own until lock-ups lift. The comparison to the SPAC boom is easy to draw, and it holds: the economics reward the people assembling the structure far more dependably than the people funding it.

The premium cost

The demand and scarcity behind these names produce premiums. Forbes’ recent article shows that the elite names trade in the secondary market well above their last primary round, with Anthropic quoted near a $1.2 trillion valuation through secondaries despite their May 2026 valuation of $965bn. Similarly, OpenAI has been trading around $908bn despite a March 2026 valuation of $852bn .

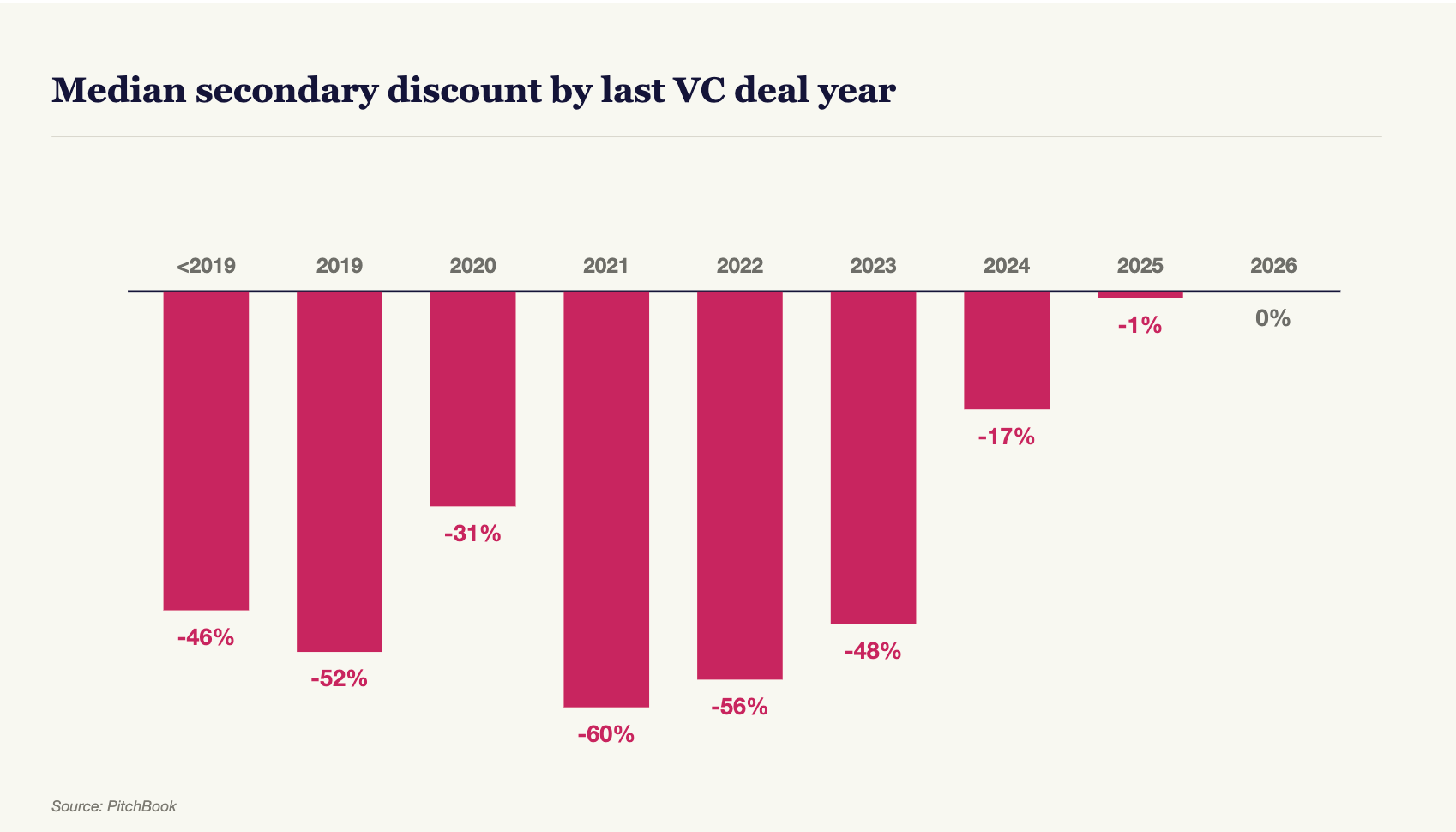

The secondary market holds more risk than the primary market, even when access is direct instead of through SPVs. There is less verifiable information on the companies being traded and there are more administrative hurdles (board refusals, ROFRs, etc.) to gain access. This market was made to be traded at a discount, not a premium. Pitchbook found that in 2021, the median secondary market discount was around 60%, in 2023 it was 48%, and today, there is no discount. However, by separating the outliers, the true discounts of the secondary market re-emerge and in structurally better opportunities than 80% of the current trades of the market.

The durable market is European tech between €500M and €2Bn

There is a segment of the secondary market that no mega-IPO can drain, that no five-layer SPV distorts, and that trades at a discount rather than a premium. It is European tech companies valued between €500 million and €2 billion.

Here, the discounts are real and durable. European venture exit value reached €67.8 billion in 2025 according to Pitchbook, still well below the 2021 peak, with exit counts falling every year since. Four straight years of frozen exits have left fund managers and employees holding valuable stakes and needing liquidity. Motivated sellers meet a shallow buyer base. European infrastructure is still developing and many of these companies are below the radar for American secondary buyers. This produces a structural discount for anyone positioned to buy. Still, above €2 billion, the European market begins to display the same crazed behavior of the American market. The prime example is Revolut’s supposed $115bn secondary valuation. Focusing on below €2 billion preserves the true value of the secondary market.

European assets also offer stability. Dealroom shows that Europe has minted 717 unicorns, a deep bench of mid-cap private names, which means there is room for liquidity to spread across hundreds of companies instead of concentrating in five. In this band, the exit routes are working. SAP alone has acquired 18 venture-backed companies since 2016, three of them in 2026, evidence that strategic buyers clear inventory in exactly this size range.

Finally, the access is clean. Buying directly offers the asset itself at a discount, without a tower of intermediaries between the investor and the company. An investor knows what they own, what they paid, and they keep the gain.

The choice investors can make

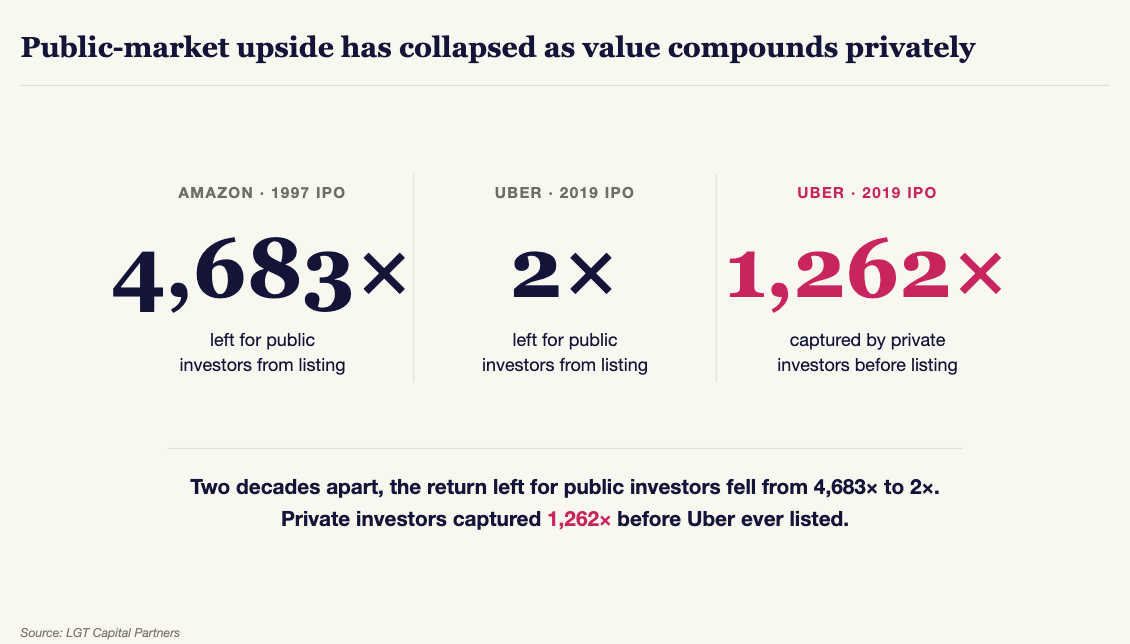

Despite the illiquidity and the obscurity of the private market, there is more value to make than in the public market.The value increasingly compounds before the listing of private companies rather than after it. When Amazon went public in 1997, public investors still had a 4,683x return ahead of them. When Uber listed in 2019, its public investors made roughly 2x while its private backers made 1,262x. The returns have moved into the private market, and they will stay there.

The question is which private-market door to walk through. One door is crowded, expensive, opaque, and about to lose its main attractions to the public exchanges. The other is a broad field of mid-cap companies, priced at a discount, held directly, with less competition and more exit opportunities than a risky IPO. The headlines are pointed at the first door. The durable market is behind the second.

To continue the discussion, share your feedback with lauren@newfundcap.com and francois@newfundcap.com.