Defense Tech: Who Owns Europe's Next Arsenal?

Defense Tech is booming, but Europe is losing the sovereignty race to US capital and slow-motion bureaucracy. The window to build independent giants is closing: it’s time to trade red tape for Ukrainian-style speed.

Helsing, a Munich-based defense AI company founded in 2021, is about to raise $1.2 billion at an $18 billion valuation. The round, led by US firm Dragoneer with Lightspeed as co-lead, was oversubscribed multiple times. Across the Atlantic, Anduril is in talks for a new round at over $60 billion, on the back of $2.1 billion in 2025 revenue and a projected $4.3 billion for 2026. Three years ago, defense was a sector most venture capitalists refused to touch. Today it is the hottest vertical in global VC, and the numbers reveal both an opportunity and a structural problem that Europe has barely begun to address.

Big Numbers, Bigger Problem

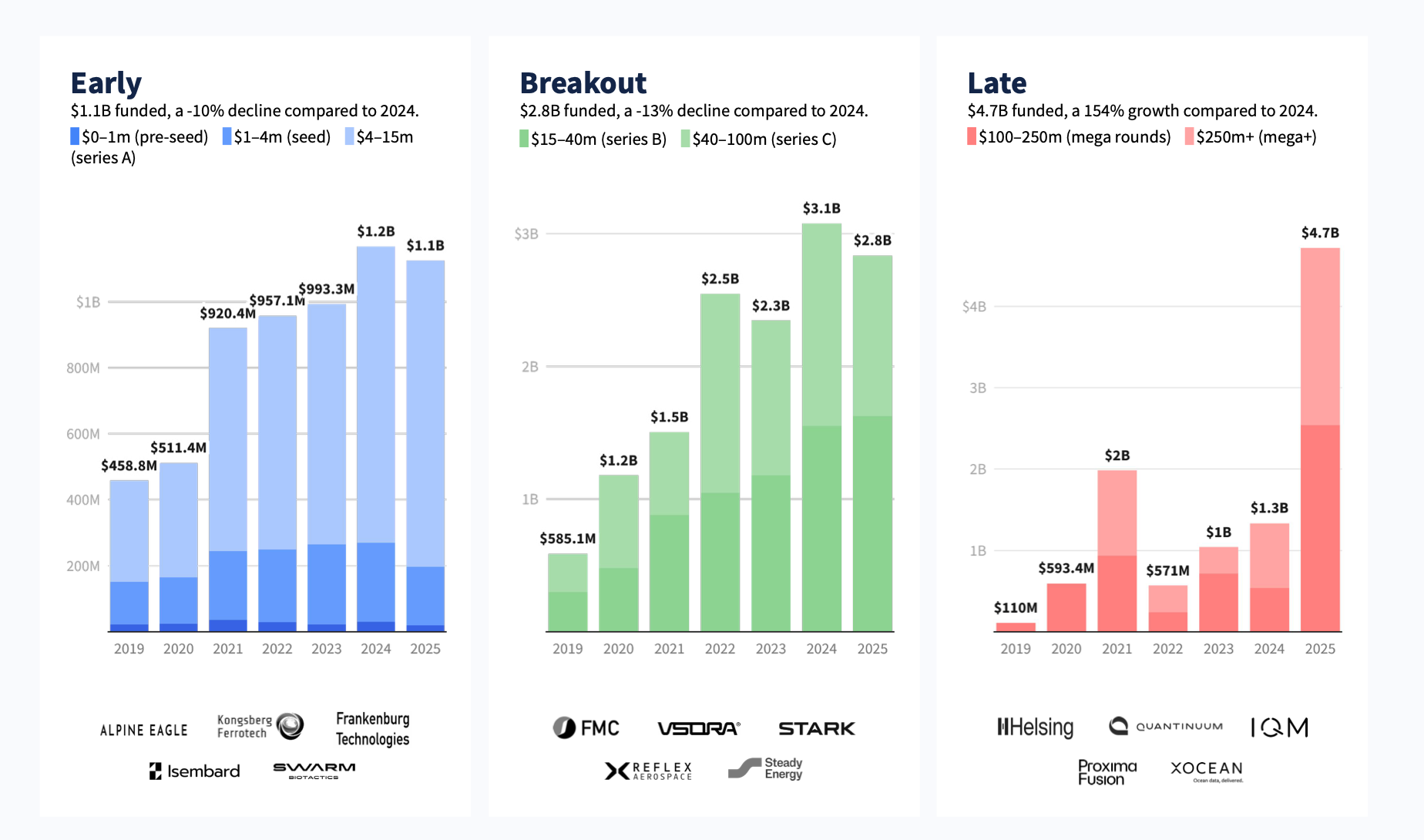

European defense, security, and resilience startups raised $8.7 billion in 2025, up 55% year-on-year and four times the level of five years ago (Dealroom full report here). Defense now accounts for roughly 10% of all European VC funding, up from less than 1% before 2020 (Dealroom report here). The number of unique investors participating in European defense rounds has risen fourfold since 2019. Specialized funds (D3, NATO Innovation Fund, Expeditions, and newer entrants like Darkstar, ScaleWolf, and Hyperion) participated in 34% of all defense rounds in Europe in 2025, nearly doubling their share from the prior year.

Europe now boasts several defense tech unicorns, in addition to Helsing: Quantum Systems, Tekever, Stark (backed by Peter Thiel). But two data points put this ecosystem in perspective. First, Anduril alone generated more revenue in 2025 ($2.1 billion) than the entire European defense VC ecosystem raised in funding ($1.5 billion in pure defense tech rounds). Second, the US captured 85% of all NATO defense VC funding since 2019. Europe's 6.2% share is growing fast, but the absolute gap remains enormous.

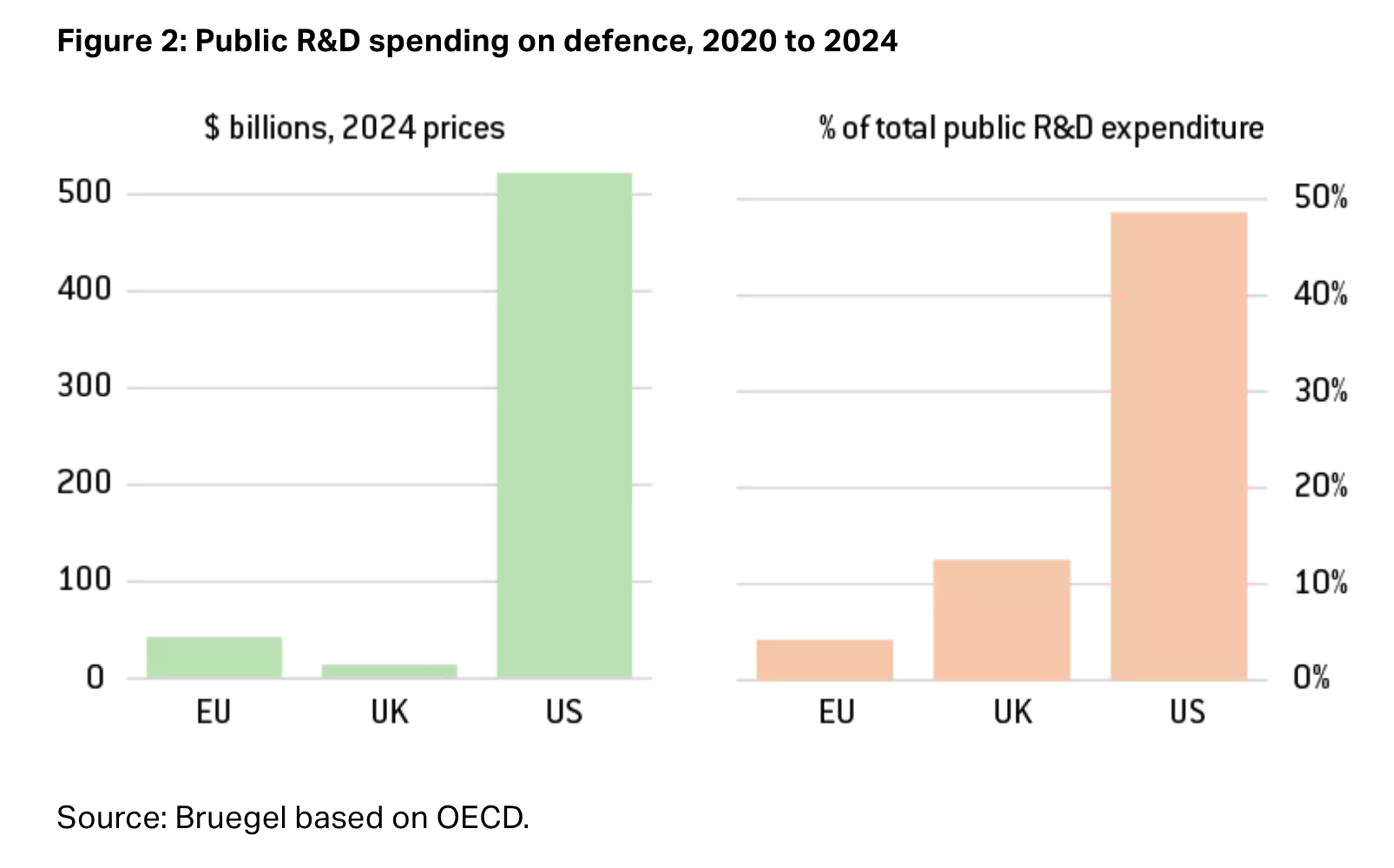

The R&D picture is even more striking. Between 2020 and 2024, the EU spent roughly $40 billion on public defense R&D. The US spent $520 billion over the same period, more than twelve times as much. As a share of total public R&D, the EU allocates 4% to defense. The US allocates 48% (more by the European Think Tank Bruegel).

European VCs aren't built for this

For a decade, most European VCs excluded defense from their investment scope, driven by ESG constraints, LP restrictions (particularly from pension funds and insurers), and a cultural aversion that treated any proximity to weapons systems as reputational risk. While they looked away, US firms like Founders Fund, a16z, and Thrive Capital built the positions in Anduril, Shield AI, and Saronic.

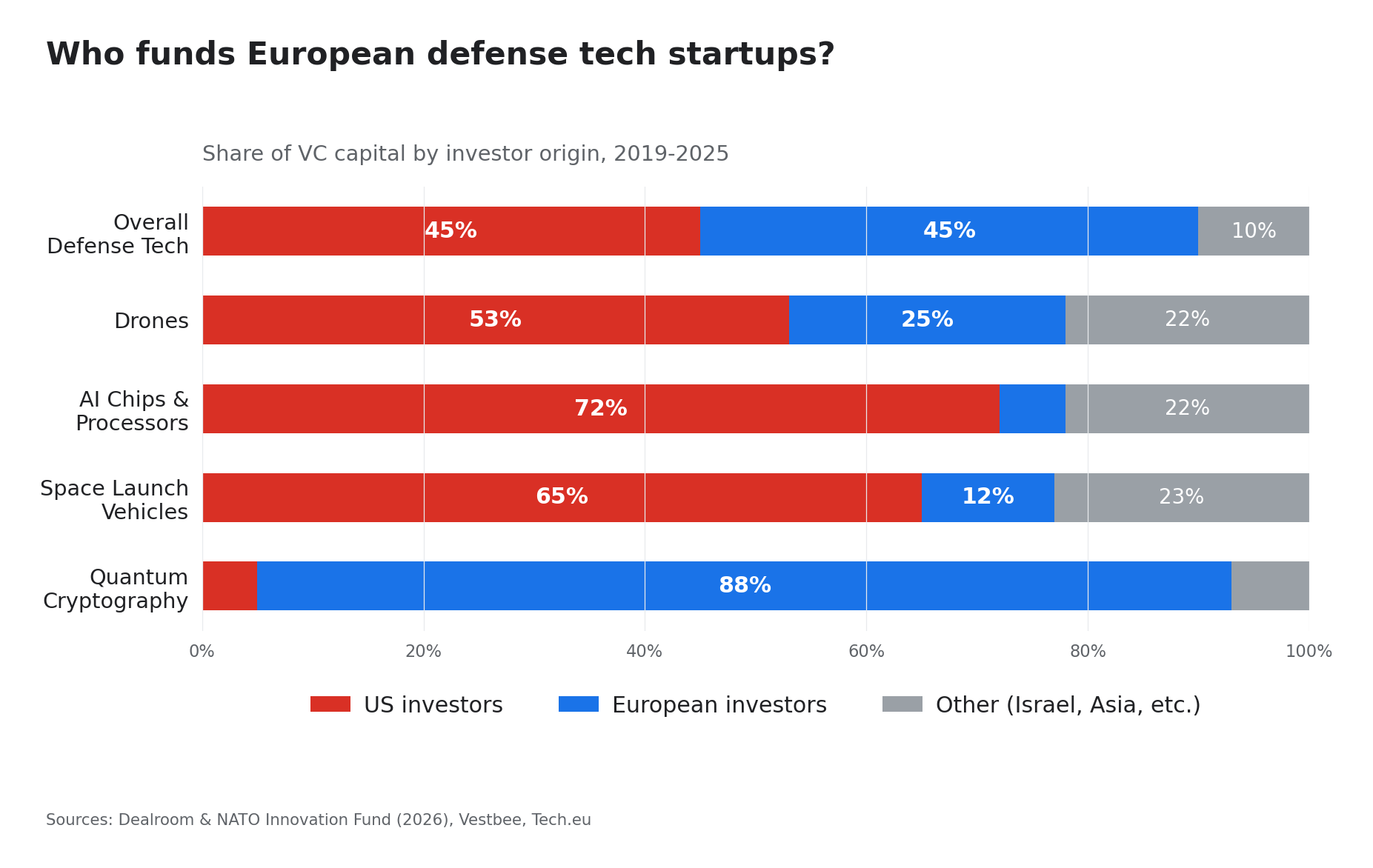

The taboo is lifting, but slowly. Today, 40 to 50% of the capital flowing into European defense tech comes from American investors. Helsing's latest round was led by Dragoneer (US) and co-led by Lightspeed (US), even though the company apparently remains nearly 80% European-owned. US VCs may already hold a veto right on key decisions. The question is how long that ownership structure holds if European VCs do not follow and who will influence decisions in uncertain times.

The picture varies sharply by subsector. In drones, US investors account for 53% of global VC funding versus 25% for Europeans. In AI chips and processors, Europe's share drops to 6%. The only segment where European capital dominates is quantum cryptography (88%), a field where Europe's research base remains strong but where commercial applications are still years away.

Adapting to defense requires more than dropping an ESG exclusion. The latest breed of VCs was built for B2B SaaS with quarterly metrics, 18-month sales cycles, and diversified customer bases. Defense operates on a fundamentally different rhythm. Procurement cycles run three to seven years. Revenue is lumpy, concentrated on a single buyer (the state), and subject to political cycles. The technology must pass military qualification processes that have no equivalent in the commercial world. Fund structures need to stretch to 12 or 15 years rather than the standard 10. LPs need to accept that portfolio construction in defense looks nothing like what they are accustomed to reviewing.

The most natural entry point for generalist VCs is dual-use technology: AI, cybersecurity, satellite observation, secure communications, autonomous systems. These companies serve both commercial and military customers, which de-risks the single-buyer problem and provides commercial revenue to sustain the business during long government procurement cycles. Helsing itself started as an AI software company before expanding into hardware (kamikaze drones, autonomous underwater vessels, unmanned fighter jets). That trajectory, from software to dual-use to full defense, is likely to become a template.

The deeper challenge is expertise. Due diligence on a kamikaze drone is not the same as due diligence on a SaaS platform. VCs need partners who understand military specifications, export control regimes (ITAR, EAR), classification requirements, and the geopolitics that shape procurement decisions. This is why specialized funds are gaining share so quickly, and why generalist firms that want to play in defense will need to hire or partner with people who have spent time inside the defense establishment.

The bear hug risk

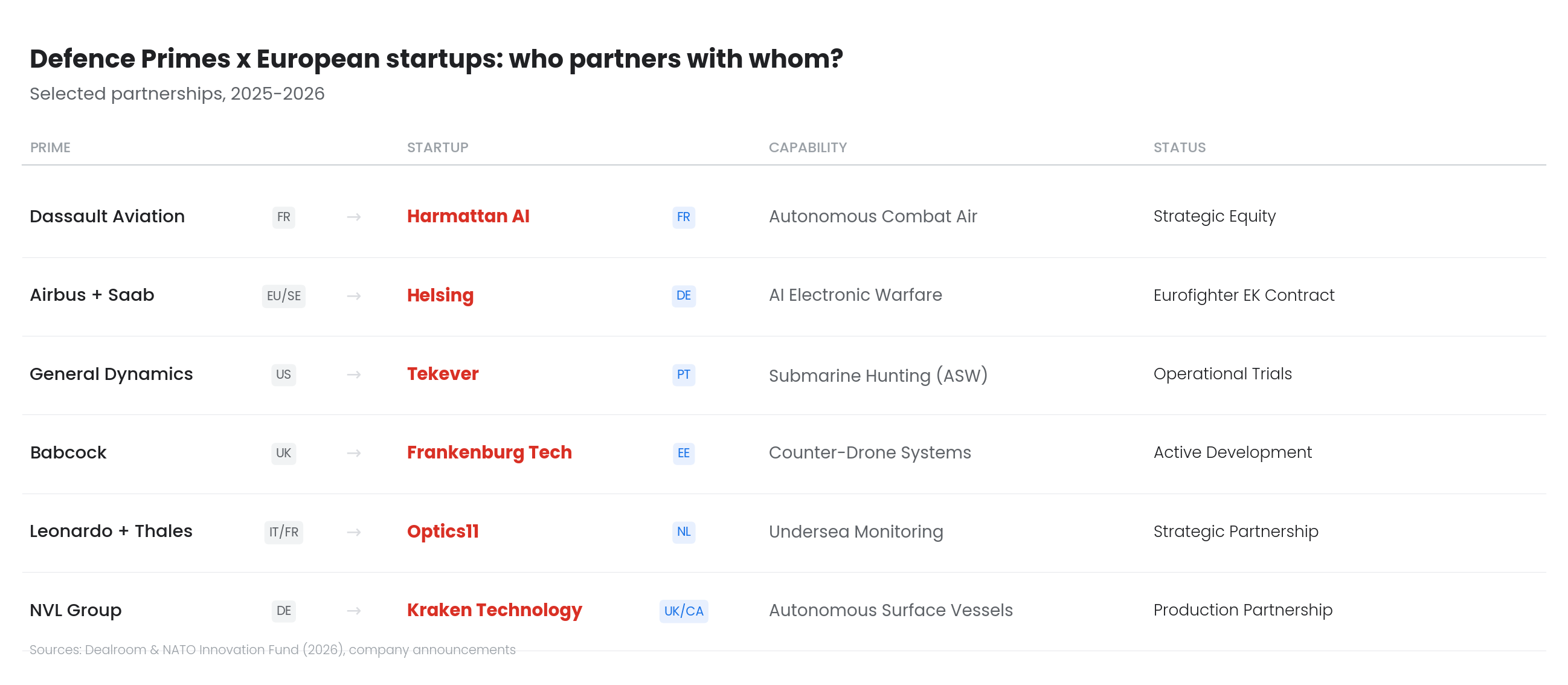

There is a third dynamic that VCs in this sector need to watch carefully: the relationship between defense startups and established prime contractors. European defense M&A hit an all-time high in 2025, four times the level of four years ago, while defense tech IPOs remained at zero. In practice, this means acquisition by a prime is currently the only exit path for most European defense startups. Helsing has struck partnership deals with Saab (on the CA-1 Europa unmanned fighter). Rheinmetall partnered with Anduril on attack drones and missile motors.

These partnerships give startups access to production capacity, government relationships, and procurement channels they cannot build on their own. But they also carry a well-known risk in the defense industry: the "bear hug," where a prime partners with a startup to absorb its technology, channel it into existing programs, and prevent it from growing into an independent competitor. Anduril chose a different path entirely, acquiring companies (Numerica's radar business, Klas, American Infrared Solutions) to build itself into a vertically integrated "neoprime" that competes head-on with Lockheed and RTX. Whether European startups can follow that trajectory depends largely on whether European capital markets and procurement agencies give them a credible alternative to selling out. Right now, with zero IPOs and fragmented national markets, many of them do not have one.

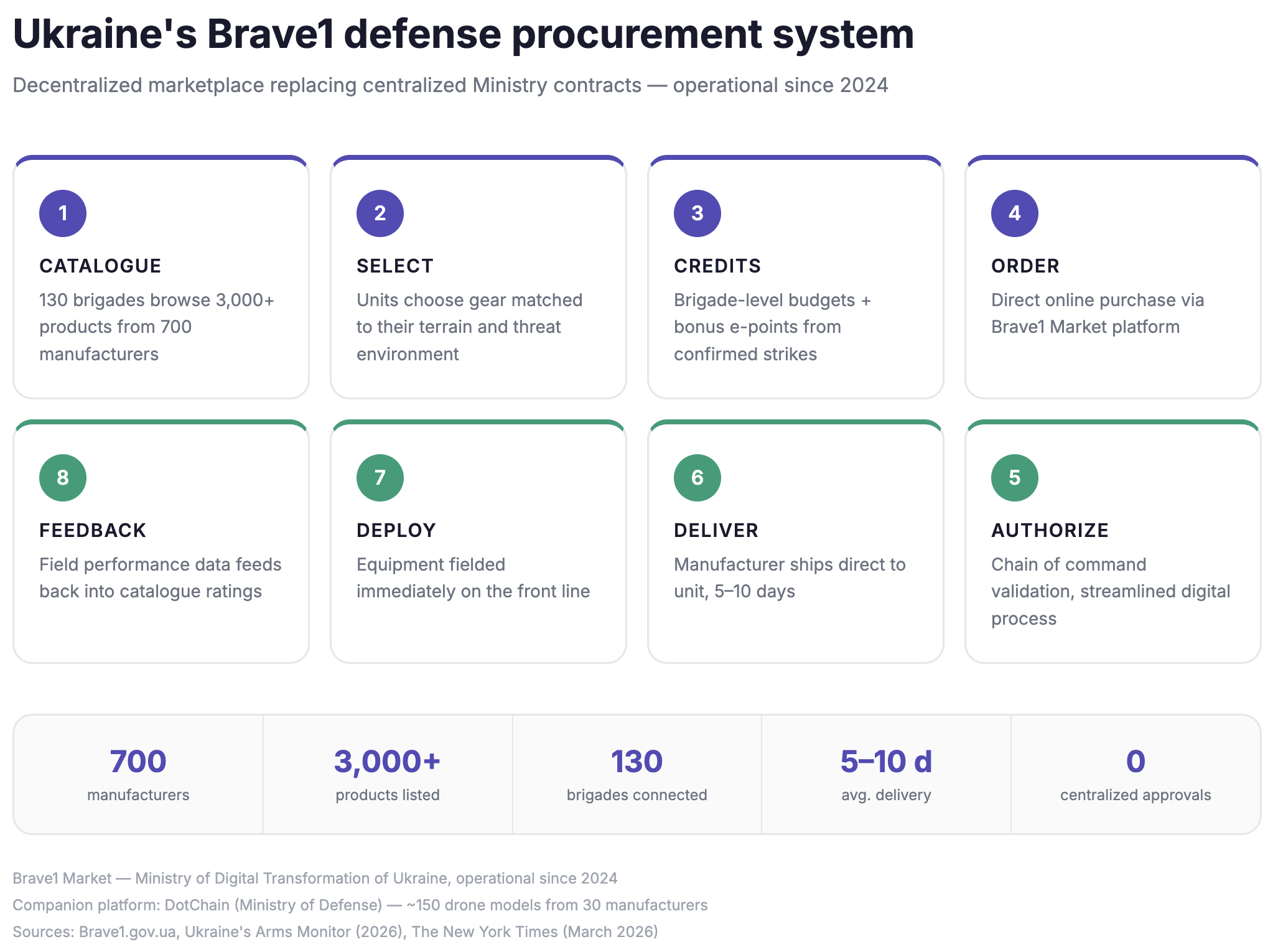

130 Brigades, 3,000 Products, 10-Day Delivery

European governments and their defense procurement agencies face an arguably harder adjustment. The systems that purchase defense equipment in Europe were designed for a world of large prime contractors, multi-decade programs, and peacetime timelines. They are not equipped to buy from startups.

The structural problem starts with fragmentation. European defense procurement operates through more than 25 national systems, each with its own specifications, qualification processes, and contracting rules. A startup that wants to sell to the Bundeswehr, the DGA, and the British MoD is essentially entering three separate markets, each requiring dedicated sales effort, different certifications, and separate government relationships. By contrast, Anduril sells into a single $886 billion Pentagon budget. That structural advantage in market size is one of the core reasons US defense startups scale so much faster than their European counterparts.

Specification only adds to the problem: traditional military procurement demands years of qualification testing against detailed technical requirements written for legacy systems. The standards were built for platforms designed to operate for 30 years, not for software-defined systems that iterate on weeks-long cycles.

Ukraine offers the starkest possible contrast. The Ukrainian government built Brave1, a defense technology marketplace created by the Ministry of Digital Transformation, where 130 brigades (nearly the entire Ukrainian military) can browse 3,000 products from 700 manufacturers and order directly using brigade-level credits (here). A companion platform, DotChain, run by the Defense Ministry, lists about 150 drone models from 30 manufacturers. Brigades choose their own equipment based on their specific terrain and threat environment, place orders online, and receive delivery in 5 to 10 days. Units can supplement their budgets with bonus points earned from confirmed strikes against Russian targets. Military analysts interviewed by The New York Times said they know of no other military in the world doing anything like it.

The system works precisely because centralized procurement failed: when drone pilots relied solely on large-scale Ministry of Defense contracts, equipment arrived in the wrong quantity or the wrong configuration, too late to match the pace of technological change on the front line. The contrast with European procurement is severe. European ministries of defense still overwhelmingly channel their budgets into a small number of massive programs (SCAF, MGCS, Tempest) that run decades late and billions over budget. Ukraine fields 3,000 products from 700 manufacturers with 10-day delivery. The average European defense procurement cycle runs three to seven years.

The European Commission launched EDIP (European Defence Industry Programme) and the AGILE pilot instrument, making approximately 1.6 billion euros available, with AGILE specifically targeting startups and scale-ups with the stated goal of bringing innovations from lab to deployment in months rather than years. France's DGA created the AID (Agence de l'Innovation de Défense) and an accelerator program supporting 28 SMEs. These are real steps, but they remain small relative to the scale of the problem and the speed at which the threat environment is evolving.

The window is closing

Both adaptation challenges come down to speed. The approach of Anduril's Palmer Luckey, building hardware at scale, integrating AI throughout the stack, and selling directly to the Pentagon with aggressive timelines, would be impossible to replicate in the current European procurement environment.

Europe has the engineering talent, the threat at its border and the budgets, or soon will. Yet Europe still lacks the institutional mindset and the institutional organization to build a proper response.

Every year that European defense procurement remains fragmented and slow, the gap with the US widens, US investors take larger positions in European champions, and the interoperability of European forces depends increasingly on American-built systems. The VC-ification of defense is already underway. Europe can still shape the outcome, but the window in which that choice remains available is closing faster than most policymakers seem to realize.

This article was written with the help of Claude (Anthropic).

To continue the discussion, share your feedback at francois@newfundcap.com.