The Largest Hidden Cost for Private Companies

European scale-ups pay the full cost of equity compensation and capture almost none of its retention value. Equity retains people only when they believe it will convert to cash within a reasonable timeframe, and in Europe, that conversion has no reliable infrastructure.

Employee equity compensation programs retain people only when they believe it will convert to cash within a reasonable timeframe. Most private companies confuse the grant of equity with the expectation of liquidity, and the cost of that confusion is detrimental.

The standard pitch is: join early, take a pay cut, receive options, and one day the paper becomes real. This worked when the average time to IPO was five to seven years. It breaks down when that window stretches to twelve or more, as it now does for many European scale-ups. The options vest, the company grows, the valuation climbs. The employee, fully vested and staring at a large number on paper, discovers it is inaccessible. No market for their shares below a €20 million minimum ticket, no platform, no timeline.

JP Morgan's analysis of a Penn Economics study puts the retention value of stock options at 95 to 275% above their granting cost. When equity stops functioning as a retention tool because there is no realistic liquidity path, that ROI collapses: the granting cost remains, the benefit disappears. According to Morgan Stanley at Work's 2025 Liquidity Trends report, 69% of private company decision-makers agree that liquidity events are important to long-term growth, and 93% say liquidity is a meaningful factor in a candidate's decision to accept an offer. The market has understood the problem intellectually. The execution, particularly in Europe, has not caught up.

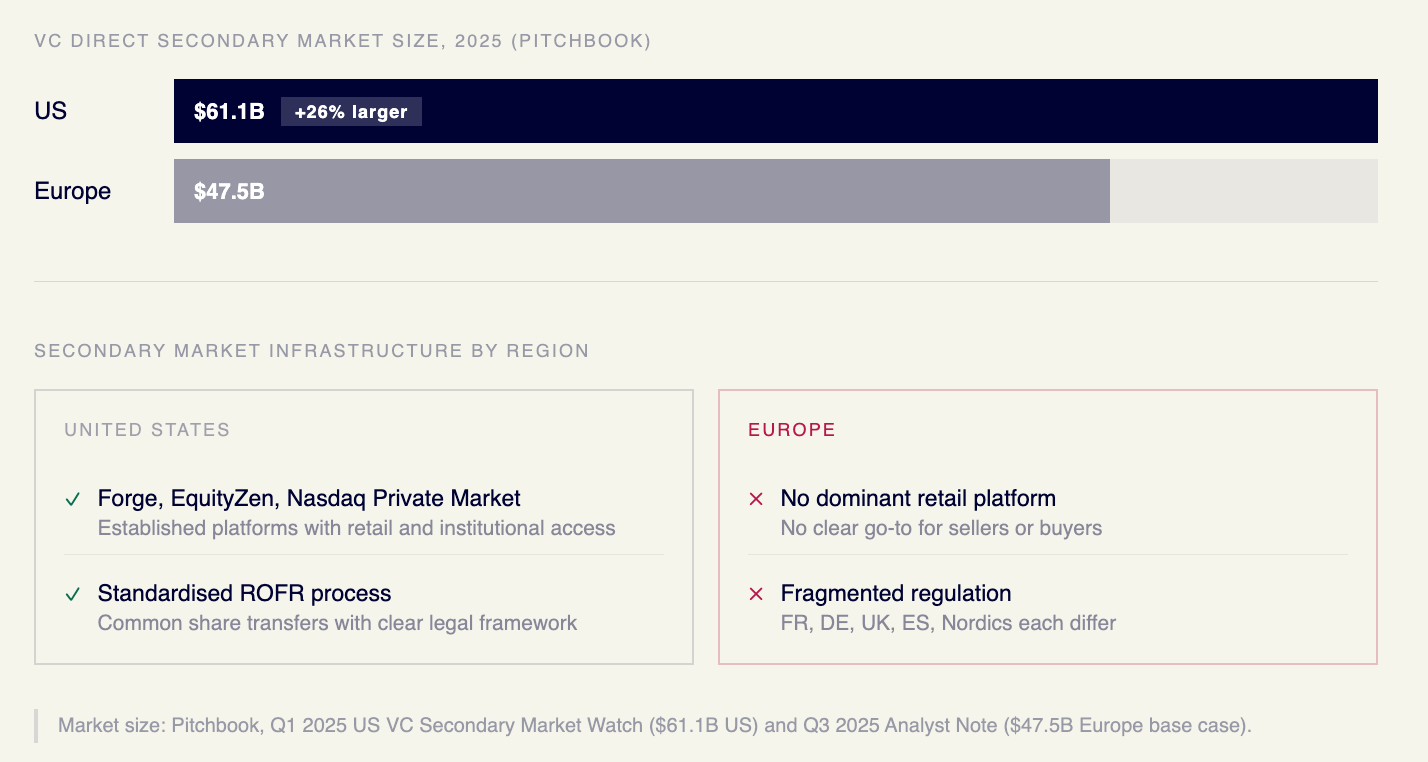

Infrastructure exists, but only in the US

Clay, ElevenLabs, and Linear have all run broad employee tender offers in the last year. Clay's co-founder Kareem Amin described the rationale plainly: the gains should not accumulate to a small group while everyone else waits. Pitchbook found the US VC direct secondary market was nearly 30% larger than Europe's in H1 2025. Preply, originally a European company now headquartered in the US, ran the most recent large-scale tender offer. It remains an exception, and for good reason: company-led tender offers require board alignment, significant legal and operational overhead, and a scale that most European scale-ups have not reached. The vast majority of employee liquidity situations will not be solved by tender offers. They require a different kind of infrastructure. In the US, that infrastructure exists: buyers, platforms, standardized processes, and a legal framework that handles common share transfers efficiently.

In Europe, nothing equivalent exists for ordinary employees. Forge, EquityZen, and Nasdaq Private Market are American platforms. European secondary brokers require minimum tickets that exclude most individual employee positions. The regulatory patchwork across France, Germany, the UK, Spain, and the Nordics makes ad hoc transactions difficult and expensive (Index Ventures' Rewarding Talent guide documents this in detail). The fiscal frameworks add another layer. In France, BSPCEs benefit from a favourable tax regime, but only at the point of sale: the longer the employee waits, the more exposed they are to legislative changes that could alter the terms. In Germany, stock options are taxed at exercise, not at sale, meaning employees owe tax on gains they cannot realise. These situations affect tens of thousands of employees across European scale-ups, and no one is building solutions for them. European scale-ups compete for talent against companies that can offer real liquidity, while being unable to offer it themselves. That asymmetry never appears in compensation benchmarks. It shows up in attrition, in declined offers, and in the quiet departure of senior engineers who choose OpenAI or Stripe over a company where their equity may never convert.

Buyers and sellers exist. Companies block the deal.

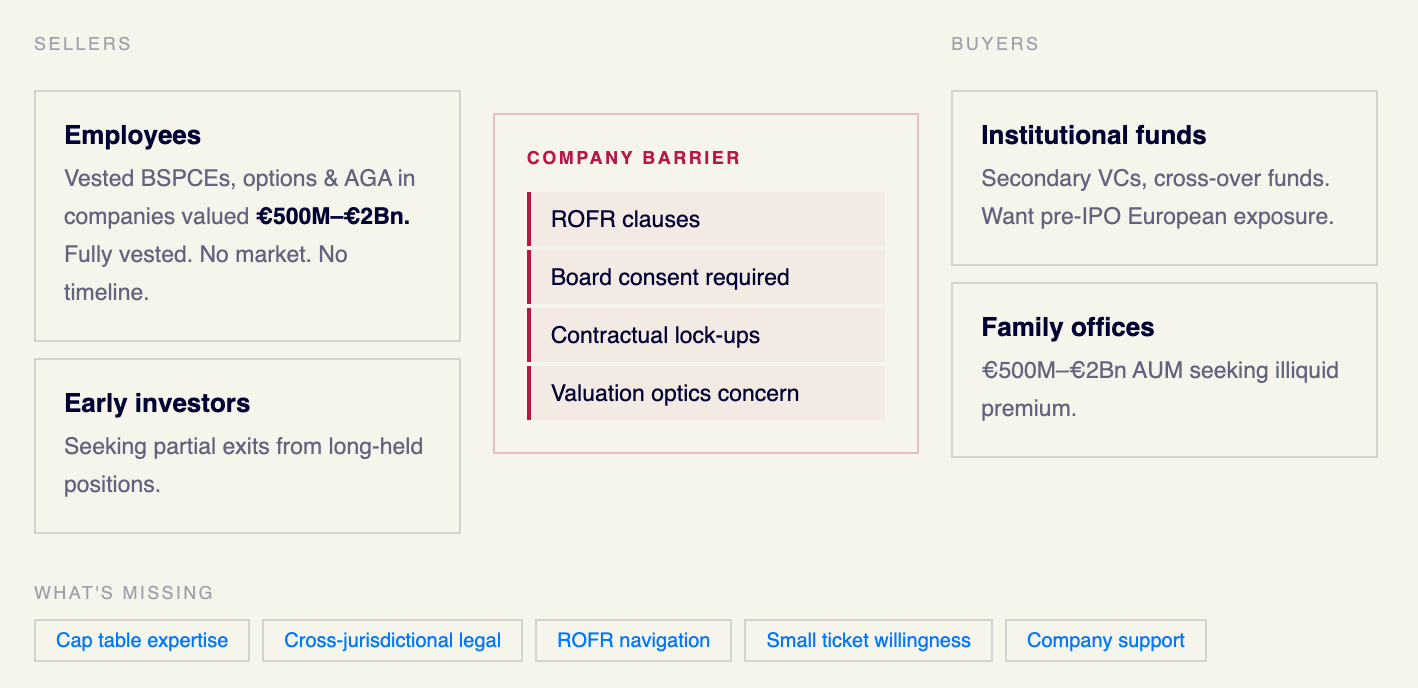

The absence of a functioning European secondary market is often attributed to ecosystem immaturity. The framing is incomplete. Sellers exist: employees with vested stock options, BSPCEs, and AGA in companies valued between €500M and €2Bn, with no structured path to liquidity. Buyers exist: institutional investors, family offices, and secondary funds who want exposure to exactly these assets. What is missing is operational infrastructure (cap table expertise, cross-jurisdictional legal knowledge, ROFR navigation, willingness to work at small ticket sizes) and, crucially, the company's support. There is a reason Forge became a multi-billion dollar business in the US. Someone built the pipes.

European companies aggravate the problem through active resistance. ROFR clauses, board consent requirements, and contractual lock-ups give them the legal tools to block transactions, and they use them. We regularly encounter executives and board members more concerned over a discounted valuation on 6,000 shares than the retention impact of a secondary transaction on the entire business.

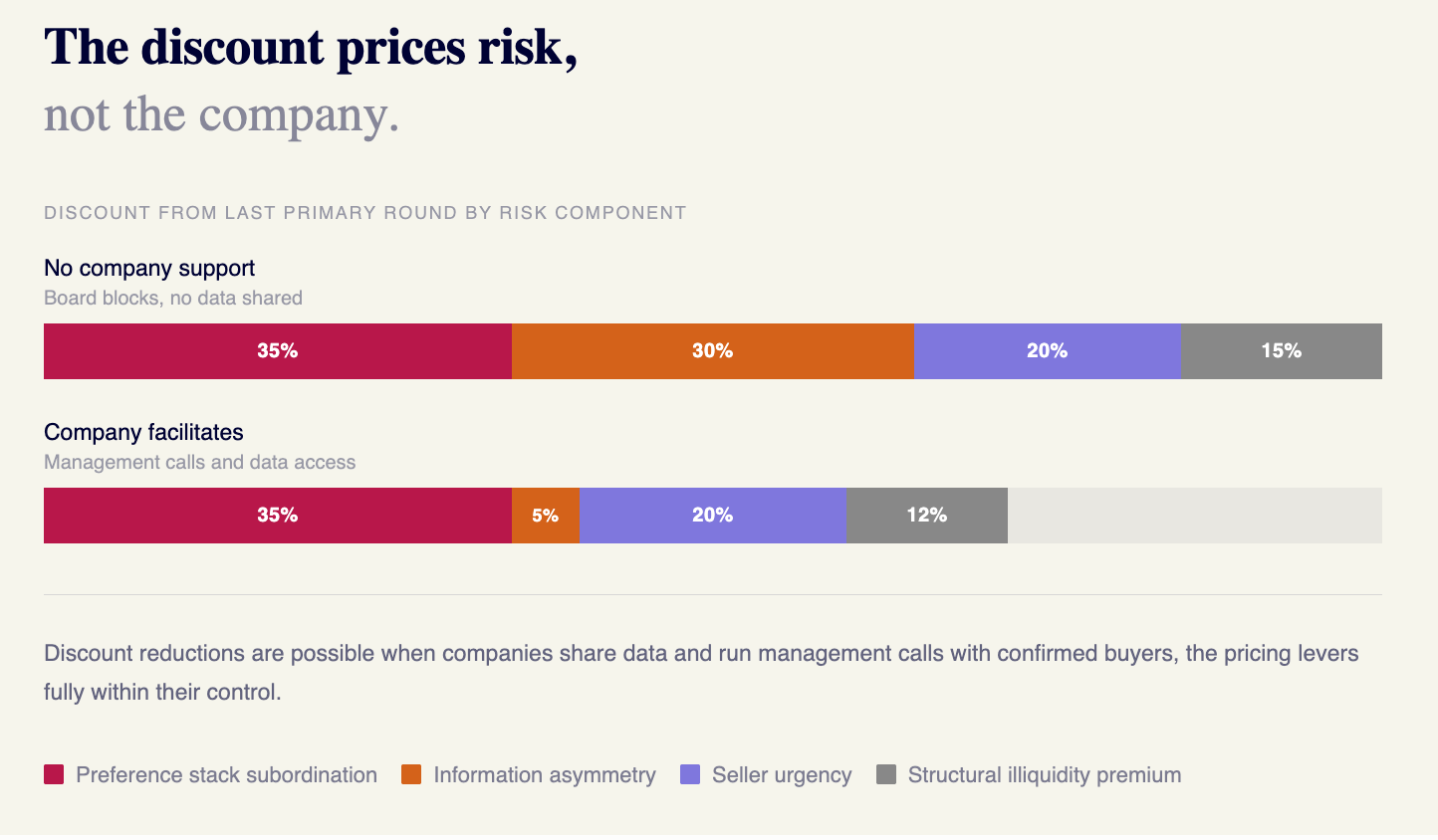

The discount prices risk, not the company

Secondary discounts do not mark the company's valuation. They price the buyer's specific risks: shares subordinated to multiple preference stacks, acute information asymmetry, and the price elasticity of sellers who often face personal urgency. Revolut used secondaries last year to raise their valuation and reduce dilution at an advantageous price, in a matter of weeks. Companies that refuse to engage will spend time fielding unsolicited approaches from buyers and frustrated employees, and miss the chance to clean their cap table on their own terms. Companies that facilitate transactions (management calls, data access for confirmed buyers) limit the discount by erasing the buyer's main source of uncertainty.

The people who leave first are the ones you need most

67% of private company employees say a future liquidity event matters in their decision to stay (Morgan Stanley at Work, 2025). That figure understates the real cost: the employees most likely to leave over illiquidity are the ones with the largest vested positions, meaning the longest tenure and the most institutional knowledge. The replacement cost of a senior engineer runs between 1.5x and 2x annual salary. For a profile earning €150K, that is €225K to €300K per departure. A scale-up losing three or four senior people a year to illiquidity absorbs close to a million euros in hidden replacement costs, before counting the loss of institutional knowledge and the signal it sends to the remaining team. As IPO windows stay closed and M&A timelines lengthen, the gap between vesting and realisation widens every quarter. Options designed as a retention tool become a source of financial stress and resentment.

The infrastructure to solve this in Europe is being built, slowly and from scratch. It will look like a network of structured bilateral transactions, not a public market. The next step is for companies to stop blocking these deals and start facilitating them.

If you'd like to continue this conversation: francois@newfundcap.com